How Consumer Culture Affects Debt Management: Reflections and Solutions for Conscious Consumption

Understanding Consumer Culture

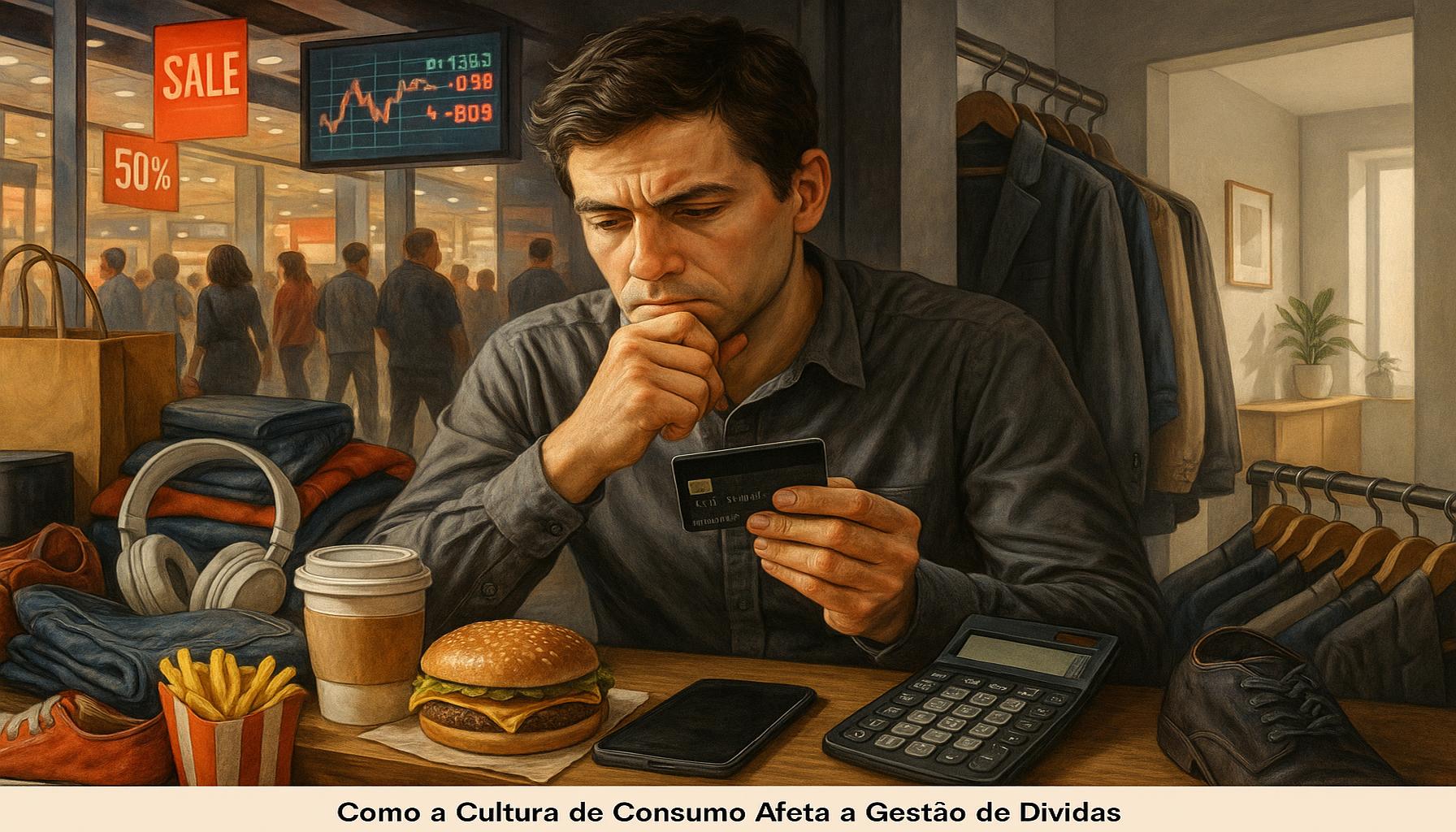

The phenomenon of consumer culture is characterized by an emphasis on acquiring goods and services as a primary method of personal fulfillment and societal participation. This culture is ingrained in the modern American lifestyle, where spending is often equated with identity and success. As a result of this belief system, individuals may find themselves caught in a cycle of overspending and accumulating debt, leading to financial instability.

Key Aspects of Consumer Culture

Several dynamics underpin the consumer culture in America, each contributing to the financial challenges many individuals face today.

- Instant Gratification: The modern consumer often desires immediate rewards, which can manifest in impulsive buying behaviors. For instance, when presented with a marketing campaign promoting a new smartphone with advanced features, an individual may rush to purchase it without considering if such a purchase aligns with their financial situation. Retailers, understanding this phenomenon, frequently employ strategies such as limited-time offers and flash sales to encourage rapid purchasing decisions.

- Social Pressure: American society frequently elevates material wealth and status, fostering a competitive environment where individuals feel the need to keep up with their peers. Social media platforms amplify this pressure, showcasing curated lifestyles that may not accurately represent reality. The desire to emulate these lifestyles can lead to unnecessary purchases, further exacerbating financial strain. For example, someone might invest in high-end fashion or luxury vehicles to project an image of success, regardless of their financial capability.

- Advertising Influence: The role of advertising in shaping consumer perceptions cannot be overstated. Aggressive marketing techniques, ranging from television commercials to influencer endorsements, often blur the lines between essential needs and superficial wants. For example, advertisements for credit cards may promote the idea of ‘living in the moment,’ encouraging consumers to spend beyond their means while ignoring the long-term consequences of accumulating debt.

Consequences of Consumer Culture on Debt Levels

As a result of these consumer behaviors, the levels of personal debt in the United States have reached staggering proportions. According to recent statistics, the total consumer debt in the U.S. surpasses $14 trillion, with millions of Americans struggling under the weight of credit card debt, student loans, and mortgages. This situation necessitates a thorough understanding of individual financial behaviors and the societal factors that encourage over-indulgence.

Strategies for Conscious Consumption

To counteract the negative implications of consumer culture, it is essential to adopt strategies that promote conscious consumption. These strategies may include budgeting, prioritizing needs over wants, and seeking knowledge about financial literacy. By creating a realistic budget, individuals can gain a clearer picture of their financial situation, allowing them to make informed decisions regarding their spending habits. Furthermore, practicing mindfulness in consumption can lead to more thoughtful purchases that align with one’s financial goals.

In conclusion, understanding the intricacies of consumer culture is vital for developing effective debt management strategies and fostering a healthier relationship with money. By acknowledging the pervasive influence of societal values on financial behaviors, individuals can take proactive steps towards achieving long-term financial well-being.

DISCOVER MORE: Click here to learn how interest rates impact your debt repayment

The Intersection of Consumer Culture and Debt Management

The relationship between consumer culture and individual debt management is profoundly intertwined. As society increasingly normalizes a lifestyle centered around consumption, individuals often find it challenging to make sound financial decisions. The allure of instant gratification and the pressures to conform to social norms can lead to a heightened propensity for debt, undermining financial stability and security.

One significant effect of consumer culture on debt management is the tendency to prioritize spending over saving. Many individuals do not fully comprehend the long-term implications of their financial choices due to the overwhelming influence of immediate desires. The marketing landscape, filled with enticing offers and promises of happiness through consumption, often obscures the necessity for prudent financial planning. This behavior not only leads to increased accruement of personal debt but also diminishes the ability to build an adequate financial cushion for unforeseen circumstances.

Financial Illiteracy and Poor Debt Management

Another critical factor related to consumer culture is the level of financial literacy among the population. A substantial portion of Americans lacks the knowledge and skills necessary to navigate the complex financial landscape, leading to less informed decision-making. For example, many individuals may not fully understand the terms associated with loans, credit, and interest rates, which can culminate in poor choices that heighten their debt burden.

- Understanding Interest Rates: Many consumers fail to grasp how different interest rates can affect the total cost of borrowed funds. High-interest credit cards can lead to spiraling debt if not managed appropriately, yet promotional offers can tempt consumers into such financial traps.

- Recognizing the Importance of Credit Scores: Consumers often underestimate the impact of their credit scores on loan approvals and interest rates. A lack of knowledge about maintaining a healthy credit score can perpetuate a cycle of debt as unfavorable terms lead to increased borrowing costs.

- Investment versus Consumption: In a society that glorifies consumption, individuals may neglect the value of investing for long-term wealth. Understanding investment opportunities can provide an alternative to relying solely on credit for financial stability.

Moreover, societal values that equate success with material possessions can further compound financial difficulties. The pressure to keep up with consumer trends may lead individuals to choose luxury items or experiences over essential expenditures, thus extending their financial strain. In such a consumer-driven environment, the relationship between personal identity and spending becomes dangerously entangled, often resulting in irrational financial behavior.

As consumer culture continues to evolve, it is imperative that individuals acknowledge its impacts on their financial health. Recognizing these patterns can serve as the first step toward implementing effective debt management strategies and fostering a more sustainable approach to consumption.

DISCOVER MORE: Click here for valuable debt management tools

The Role of Digital Consumerism in Debt Accumulation

In recent years, digital consumerism has emerged as a significant force shaping consumer behavior and debt management practices. The pervasive use of online shopping, coupled with the rise of mobile payment solutions, has revolutionized how individuals engage in purchasing activities. While these advancements offer convenience, they also encourage impulsive spending behaviors that can lead to increased debt.

One of the primary concerns with digital purchasing platforms is the prevalence of “buy now, pay later” services, which enable consumers to acquire goods without immediate payment. While these services may seem beneficial, they often obscure the total cost of purchases and promote a cycle of dependency on credit. Research indicates that individuals utilizing these payment options tend to spend significantly more than they would through traditional retail channels. The ease of access and instant gratification further complicate consumers’ ability to assess their financial limits.

Impulse Buying and Emotional Spending

Compounding the issue of digital consumerism is the influence of social media advertising and peer comparison. Platforms like Instagram and TikTok often portray lifestyles centered around luxury goods and experiences, fostering a desire for instant gratification. This constant bombardment of curated content can lead to impulse buying—a phenomenon where consumers make unplanned purchases driven by emotional responses rather than thoughtful consideration of their financial situations.

- The Role of Influencer Marketing: Influencers frequently endorse products and services, creating a disconnect between the perceived value of these items and their real financial implications. Consumers may feel pressure to emulate these lifestyles, leading to spending that does not align with their financial reality.

- Gamification of Shopping: Many e-commerce platforms employ gamification strategies, such as reward points and flash sales, to entice consumers into making rapid purchases. While these tactics can enhance customer engagement, they can also accelerate regrettable spending, placing individuals further into debt.

- Delayed Gratification vs. Instant Gratification: The rise of digital shopping has shifted expectations regarding consumption behavior. Many individuals no longer practice the art of delaying gratification, which can lead to financial strain. This shift further complicates effective debt management, as individuals may fail to prioritize saving or budgeting in light of immediate wants.

Developing Conscious Consumer Habits

Given these challenges, it is crucial that consumers foster conscious consumption habits to combat the pitfalls of consumer culture and digital spending. Engaging in mindful practices can significantly impact debt management outcomes and promote long-term financial health. Here are several strategies to consider:

- Creating a Budget: Establishing a detailed budget can help individuals track spending patterns and distinguish between needs and wants, thereby mitigating impulsive purchases.

- Implementing the 30-Day Rule: Encouraging a waiting period before making significant purchases can reduce impulsivity. This approach allows consumers to assess whether a particular item is truly necessary.

- Educating Learning: Increasing financial literacy through workshops or online courses can empower individuals to make better financial choices, ultimately reducing debt accumulation.

- Limiting Exposure to Advertising: Taking steps to minimize exposure to marketing messages, such as unfollowing influencers known for promoting excessive consumerism, can help individuals maintain focus on their financial goals.

In light of the pervasive nature of consumer culture and its impact on debt management, adopting conscious and deliberate consumption strategies is essential for maintaining financial wellbeing. By addressing impulsive behaviors and embracing informed decision-making, individuals can take proactive steps toward achieving greater financial security.

DISCOVER MORE: Click here to learn about choosing the right card for your financial profile</

Conclusion

In conclusion, the intersection of consumer culture and debt management presents a complex landscape that requires urgent attention from individuals and society at large. The advent of digital consumerism and the pervasive influence of social media have not only transformed shopping habits but also intensified the tendency towards impulsive spending and emotional purchasing. As the data indicates, the ease and accessibility of credit options, such as “buy now, pay later” services, have further exacerbated financial irresponsibility, often leading consumers into unmanageable debt levels.

To counter these adverse effects, embracing conscious consumption is imperative. By implementing strategies such as budgeting, the 30-day rule, financial education, and reducing exposure to marketing messages, individuals can reshape their spending habits and reinforce their financial health. Mindfulness in purchasing decisions allows for a clearer distinction between needs and wants, essential for effective debt management.

Ultimately, fostering an awareness of the emotional and psychological triggers driving consumer behaviors is vital. As individuals commit to cultivating these intentional habits, they not only enhance their own financial wellbeing but also contribute to a more sustainable consumption culture. By prioritizing thoughtful spending and resisting the pressures of consumerism, society can move towards a future where financial resilience is attainable for all.

Related posts:

How Banks Influence the Financial Market and Credit

Debt Consolidation: Is it Worth It to Unify Your Payments?

How to Protect Your Investments Against Inflation in the USA

The Role of Financial Intelligence in Wealth Building

Practical Tips for Creating a Budget to Help Get Out of Debt

Financial Planning Tips for Retirement in the USA

Linda Carter is a writer and expert in finance and investments. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the Oracle Lifes Ciences Inform platform. Her goal is to provide readers with practical advice and effective strategies to manage their finances and make smart investment choices.